All published articles of this journal are available on ScienceDirect.

Motivation and Commitment as Influential Factors in a Taxation Department and the Way They Affect Employee Performance: A Survey Study in a Taxation Department in Indonesia

Abstract

Introduction:

Tax revenues in each country cannot be fully collected depending on the planned targets without good work, which is influenced by individual performance. This means that taxes collected at the Tax Department in Indonesia depend on worker performance as one of the main factors affecting the expansion of national revenue.

Aims:

Just like in any other organisation, employee performance of Indonesia’s taxation unit is influenced by established standards, which determine the quality of work, completion of targets and of course instilling responsibility in employees who are required to demonstrate such values through the implementation of the predetermined work procedures and policies. This study is a survey which uses a descriptive method. The descriptive method involves the assessment of research variables, which aims to determine the relationship between such variables and their influence on the findings of the study.

Conclusion:

The results revealed that motivation and commitment in the taxation department fall in the category of 'good enough', though without optimum performance. During verification, it was revealed that there is a positive and significant influence on performance which is partially influenced by commitment and motivation; however, competence was one of the other key factors.

1. INTRODUCTION

Throughout the world, taxes continue to be regulated by governments. Governments actively encourage their citizens to be tax abiding citizens. However, though governments do all that they can to collect taxes, the working force is essential to the process. With this in mind, several studies on worker performance have examined and explored a broad set of potential performance measure determinants among workers [1] in taxation departments, as the main public accounting unit of any country regarding revenue collection and responsible for monitoring public accountability.

Human resource performance is of great importance to good production in any company or organisation, be it government or private, including in the taxation department. However, the specific hardships and challenges faced may differ from one taxation department to another, depending on the nature of the work [2]. Overall, the transformations of tax administration all over the world are influenced by two inexorable forces [3], which include, firstly, the move away from a command and control model built on the repression of illegal behavior to one predicated substantially on voluntary compliance. The other factor of change is the increasing induction of managerial and client-centric values in public management [3]. This means that as the world changes, and as public management calls for hybrid models of service delivery, tax administration is expected to change its approach from forceful attitudes into the treatment of taxpayers as customers or “clients” who must be respected and treated with courtesy [3].

Though motivation and commitment are generally considered management topics, in this present study, they have been discussed from the accounting perspective, with the aim of understanding how a taxation department can function with a motivated and committed human resource in relation to public revenue management and accountability. In one of the studies conducted by the OECD regarding taxation, it was established that most of the revenue bodies were periodically surveying their staff to learn their levels of satisfaction, engagement, motivation, competence, and performance [4], and of course to know their level of commitment.

Osinski, Lethbridge, and Hinsz [5], in their study carried out on behalf of USAID, established that given the heavy reliance on personnel to perform core duties and the fact that the wage bill for staff often exceeds 80 percent of total operating costs, human resource management is a key issue for tax administrations [5, 6]. Studying human resource from an accounting perspective is important for the handling of taxation data. In most cases, tax administrations are in possession of a huge amount of tax-related data that can be re-used for the benefit of taxpayers [7]. This is usually the job of a public taxation accounting officer, who must know the specific process for this context as it is not done in the same way that private banks and wealth managers operate [7].

In this regard, countries such as Indonesia have regulations in place to smoothly handle issues regarding public accountability. Taxes are regulated through government policies. The basis for this lies in the 1945 Constitution, which specifies that all taxes and other charges are to be managed by the government. In the case of this paper, public accountability in the taxation department is enforced under Article 23 (1) [8] of the constitution.

However, less is known about how [9] the Republic of Indonesia manages its human resources through the taxation department. Though the government has put in place the Directorate of Taxes, it is still difficult to collect domestic revenues [8]. This is evidenced by the government’s collected tax ratios, which do not seem to be increased significantly. However, Indonesia’s measure for taxes is conducted based on the same system as used by the rest of the world [9]. By looking at the sample of tax [9] from other developing countries of equal status, Indonesia has been able to reach a tax ratio of 20%. On the other hand, despite several changes ranging from revenue and tax base expansion, tax amnesty, and improvement of other financial services and infrastructure, Indonesia currently has little to be admired, hence the need to investigate the commitment and motivation of human resources. Nevertheless, tax amnesty has yielded some returns, as shown in Table 1 below.

| Tax Amnesty Targets | Tax Amnesty Achievements |

|---|---|

| The use of repatriated assets for economic purposes. | The government received IDR 147 trillion, which is equivalent to $11 billion and makes up 14.7% of the IDR 1000 trillion. |

| An expansion of the taxation database. | A large number of newly registered taxpayers joined the program. |

| The increment in both the short-term and long-term revenues through taxation. | IDR 134.55 trillion was collected as tax revenue, and IDR 4.884 trillion was declared in new assets. |

From the table above, it can be observed that when using asset repatriation as an economic growth performance indicator, as reflected between 2016 and 2017, Indonesia’s tax ratio increased-though below the government target. It is noted that taxpayers who joined the programme, which led to the expansion of the tax base, were 956,793 out of the 36 million officially registered taxpayers across the country. Out of this, 956,793, 53,000 were registered during the programme and IDR 134.55 trillion was collected. Assets that were at least equivalent to IDR 4,884 trillion were declared [10].

The above summary symbolises the importance of staff commitment and motivation in accelerating a country’s development and growth. In a human development report from 2013 by UNDP [11], it was noted that with efficient human resources, countries can accelerate their achievements in the education, health, and income dimensions, as measured by the Human Development Index [11]. Aguinis and Kraiger [12] have pointed out that, as organizations struggle to compete in a present global economy, differentiation on the basis of the skills, knowledge, and motivation of the workforce has increasingly become important. The purpose of this paper is to describe the importance of commitment and motivation in good tax management and its holistic handling from an accounting perspective, which is an important human resource concern in any accounting department of any given country.

2. LITERATURE REVIEW

A motivated and committed human resource in a taxation department of a nation is critical to achieving expanded tax revenue and improved economic growth. A proper working environment may encourage the staff to work in good faith for the good of the country. Faithful, motivated, and committed workers will likely lead to an increased income for the country and a reduced budget deficit, which in the long term will increase national saving [13] and promote improved economic growth. In a study by Puspitasari [14] on motivational postures in tax compliance decisions (2014), she mentions five motivational postures categorized as important in the context of taxation: commitment, capitulation, resistance, disengagement, and game playing. From the five motivational postures, she points out two postures that reflect an overall positive orientation to authority: commitment and capitulation [14]. Motivation and commitment can help to dislodge and prevent leakages, conspiracies and intrigue between rogue taxpayers and rogue tax officials, preventing the use of fake finance validation systems [13].

Due to the importance of the human component in tax collection, in 1983 Indonesia changed its method of handling taxation issues. Rahman [15] notes that Indonesia’s desire to improve its tax system is reflected in the establishment of various tax reforms which started in 1983, including changing the tax collection system from official assessment to self-assessment [15]. Self-assessment shows how important the motivation and commitment of an individual is in improving a taxation department.

However, proper regulations are required due to the uncertainties caused by some other factors, which may include the increased and improved remuneration of workers. Motivation in employees is necessary for carrying out their tasks, which can lead to the achievement of organizational goals [16]. Consisting of intrinsic motivation and extrinsic motivation, motivation overall plays an important role in an organization forming the commitment of its employees [2].

Commitment is one component of motivation. According to Gangl et al. [17], committed motivation represents intrinsic motivation, whereby taxpayers feel a moral obligation and responsibility, to be honest while performing their duties [17]. If this form of motivation is intrinsic within the taxation department staff, it means they will perform their duties without any form of compulsion.

Hofmann, Hoelzl and Kirchler [18] have pointed out that taxpayers' willingness to cooperate with the government and its institutions generally depends on a number of variables [18], including a motivated and committed staff. Organizational challenges, specifically for the human resource department, are related to maintaining a motivated and committed staff [19, 2].

From the M and E Studies (Accessed June 2018), it has been revealed that the more committed and motivated workers are, the higher the probability of achieving the established organizational objectives, hence enhancing work performance [19]. As all government institutions are served by human beings, motivation and commitment cannot be underestimated since they both directly have an impact on the organization’s performance and effectiveness [19, 2, 5, 6, 10].

For the state to collect revenues in an efficient and cost-effective manner [20] through taxes, it must ensure a healthy [20] working human resource. A healthy human resource helps to reduce tax evasion on the part of citizens [20], which might be brought about by an inefficient tax department. Though the motivation and commitment of the staff are fundamental in tax collection, there are other measures that can be adopted [21] to help increase and expand the tax base of a country. According to Leder et al. [21], such measures include a deterrence policy, which can act as a suitable strategy to promote tax payment by citizens. The taxation workforce is not only required to take a lead [22] in maintaining good performance but also must provide the evidence base needed [22] for the expansion of the tax base by avoiding poor behaviors-for instance, cooperating with tax defaulters.

It is due to the importance of human resources that I examine the importance of motivation and commitment as fundamental factors in improving the performance of workers in the taxation department.

3. METHODOLOGY

In this section, the methodology is discussed. The researcher applied a survey research method alongside a descriptive verification approach, which was used to determine the relationship between variables. Survey research is used to obtain data which is then used to determine the specific characteristics of a group [23]. For this study, the survey method was chosen due to the fact that taxation-though it appears common in all countries-has varying characteristics, which this research framed into the variables of motivation, commitment, and worker performance.

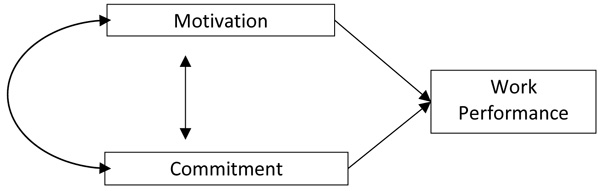

The descriptive method uses assessment of research variables. Verification is achieved through path analysis, which aims to determine the relationship between the research variables, as well as test the hypothesis. This study utilizes a quantitative method with descriptive and explanatory approaches, describing the characteristics of the variables being studied while undertaking verification tests regarding the hypothesis. The unit of analysis in this study is employees of the Directorate General of Taxation at the Regional Office of South Kalimantan. The study was conducted on a sample of 140 respondents, selected from the staff within the taxation office of South Kalimantan Province. Fig. (1), below, briefly illustrates the three common variables.

The above illustration shows that there are three variables: motivation and commitment, which are assumed to influence work performance. The researcher has excluded other factors from the discussion and illustration, though they might be fundamental. The illustrated factors are simplified for three reasons: to ensure that flow of the research is clear and not misleading, to allow us to easily understand the responses of respondents who participated in the research, and to involve a sufficient number of participants or respondents [23] who are able to facilitate the easy completion of the research.

Borrowing from Fraenkel and Wallen [23], the researchers applied a survey technique because it involves open-ended discussions and responses which can be used with greater confidence and focus regarding specific topics and discussions [23], so there is no wastage of time and resources.

4. RESULTS

4.1. Commitment

During the data analysis, it was established that most respondents have no commitment to their work. This is found in repetitive answers to the survey which are also reflected in acts represented by an indicator of employees who left their job in comparison to those who demanded compensation for each success and achievement attained at work. In the survey, it was established that employees in the taxation departments across Indonesia, including in South Kalimantan Province are paid depending on the number of taxpayers served per individual. Most respondents showed dissatisfaction with such form of compensation, thus acting as an indicator contributing to low commitment, hence dissatisfaction among employees.

In an effort to learn whether individual employees in the organization meet the criteria of efficiency and effectiveness, there were measurements. The outcomes were then analysed based on the existing standards. Since, the present study was on individual employees, the level of efficiency and commitment was measured based on individual capacity.

The authors look at efficiency from the individual performance in association with the taxation standards system. While effectiveness and commitment are taken as individual feelings and attachment to the company. Effectiveness has been related to organisational performance. The performance was basically perceived from the aspect of how taxes are collected, and the targets set for each participating respondent in this study.

In this paper, it has been established that employee performance is measured in relation to individual commitment among workers. The component of perseverance, persistence and devotion was taken as determining indicators. Employee performance is a psychological process which is more to people’s work behaviour and attitude towards effective productivity. Though there are differences among employees, they rotate around positive feelings, commitment and the feeling of attachment to the company and lastly perseverance of individual employees. In other words, differences among individual employees exist due to nature and circumstances. It is this situation which helps to determine employee’s satisfaction or dissatisfaction within a working environment. The final findings on this point, therefore, concludes that commitment being individualistic, it is this individual aspect which helps in motivating workers, hence influencing performance.

From a commitment perspective, the study analysis revealed average performance with a falling value in the category of pretty good to very good. This meant that most of the respondents performed well. Hence, indicating better worker performance, since employees have a high feeling of attachment, perseverance and devotion to their job. It was established from a social perspective, there are strong bond feelings of attachment and responsibility among the taxation workers in Kalimantan.

4.2. The Influence of Work Discipline and Competence on Motivation

In summary, based on data processing results, worker compensation and one’s competence were of the same coefficient value, compared with the work discipline aspect or variable. In this regard, it is therefore interpreted as:

- Work discipline as a variable has a certain degree of contribution to motivation. This means that workers, with good discipline at work, contribute to individual motivation. This may also influence the compensation received by employees from their employer.

- There is a contribution from the competence variable to work motivation of the employees. This means that competence variable contributes to work motivation of an employee within an organisation.

- However, there are other factors which influence work performance besides the mentioned variables.

Regarding the above summary, it has been found that there is a simultaneous influence of the variables of work discipline and competence on work motivation at a value of 62%. It, therefore, implies that 62% of the motivation variable can be explained by the work discipline and competence variables. The remaining 38% is influenced by other factors.

4.3. Employee Motivation

According to survey findings, it was found that commitment, positive reinforcement and work motivation are influenced by other factors, which direct and indirect influences. Factors influencing employee motivation directly were discipline at work, whereas the other indirect variable was positive enforcement which took on the form of reward. However, the findings further revealed that direct influence has less impact motivation when compared with the indirect influencer. Meaning that both direct and indirect factors positively impacted on employee work motivation. The other factor such as compensation and devotion were reported to either directly or indirectly affect work performance and motivation. It was finally, concluded that there is a direct impact on employee work motivation. The research also revealed that competence is also one of the variables that affect the work motivation variable either directly or indirectly. The direct influence of the competence variable on work motivation is categorised as significant, while the indirect influence through two other variables, i.e., the work discipline variable and compensation are categorised as average. Hence, concluding that the direct influence of competence on employee work motivation is higher than the indirect influence.

According to the above summary, it is then interpreted that partially individual influence is affected by the competence variable which affects one’s work motivation. This shows that positive enforcers such as worker compensation and Behavior influence motivation. Depending on this form of findings, it is then concluded that improving employee motivation can be attained by improving employees’ competence, through the provision of positive enforcers which are proportional to individual work discipline and devotion. It is therefore concluded that, if all requirements were to be met, then the motivation of employees would automatically improve.

Besides motivation and commitment, work performance among taxation workers in South Kalimantan is also affected by other factors. Other factors are represented by 40% variables. Such other factors may include: job promotions, efficient and effective communication, behaving well at work, family background and nationalism spirit among others.

4.4. Reward and Individual Capacity on Commitments

Based on the survey results regarding this point, it can be deduced that compensation has the highest contribution, compared to the other variables such other work discipline, competence and motivation. This leads us to the interpretation that:

- There is a degree of contribution from the discipline variable to work commitment of a larger magnitude. Meaning that higher employee working discipline contributes greatly to commitment.

- There is a degree of contribution from the compensation variable to commitment and compensation received by the employee will contribute to commitment significantly.

- It is lastly noted that there is a degree of contribution from the competence variable to commitment, with an average magnitude.

Going by the given summarised perspective, we find a combined influence of variables which include: compensation as a reward factor and competence as an individual capability factor affecting commitment amounts positively at a degree of 62%. Implying that the existing variance in commitment can be explained by 62%. While the remaining 38% is said to be influenced by other variables.

4.5. Employee Commitment

In the analysis of survey results, it was established that there is both a direct and indirect influence of variables of work discipline, compensation, and competence on commitment. The direct influence came from work discipline, whereas other indirect were compensation and competence. It was finally found that the discipline of workers as a direct influence had little influence on commitment, while the indirect factors significantly influenced commitment from the employee commitment perspective. Hence, being concluded that both direct and indirect influence are of influence on employee commitment.

Reward in the form of worker compensation is said to be another variable that impacted on commitment- it has been found that the direct impact of compensation on employee commitment has a greater influence than the indirect factors. This means that affirmatively both the direct and indirect factor are of compensation affecting employee commitment.

Individual capacity in the form of competence is taken as another variable that influences the commitment of an employee. There is a direct influence of the competence on commitment while on the other hand, there are other indirect influences of variables. However, on this aspect, it has been concluded that the direct impact of competence on employee commitment is of significant impact compared to the indirect influence.

Going by the above summary on the findings, it is then concluded that the largest partial or individual influence on commitment is compensation. However, competence and work discipline are said to affect motivation. In relation to such results, it can, therefore, be concluded that improving commitment of employees can be achieved by increasing the compensation received by each employee. It is evident that with a good employee welfare, there will be an individual initiative to a commitment to improving work performance, hence providing the best of their services to the company. Other variables basically follow the individual abilities of the employees.

In summary, though we focus on two variables for this research, there are other many variables that affect commitment, as shown by the influence of variables outside the model. It, therefore, implies that the influence on commitment can also be from other variables not covered in this research.

4.6. Work Motivation and Commitment

In the analysis the correlation and coefficient undertaken, it was found that work motivation and commitment to employee performance could be obtained based on the following summarised interpretation, that:

- There is a level of contribution from the employee motivation to the performance of employees to a certain magnitude. This implies there is a higher work motivation of employees which greatly contributes to employee performance to a higher degree.

- There is a level of contribution from the commitment to the performance of employees at an average category of performance. This means that there is a higher commitment by employees contributing to worker performance to a certain degree.

According to the above summary, from both the analysis of correlation and coefficients, it is concluded that there is both direct and indirect influence of work motivation and commitment on employee performance with an organisation, such as the taxation department.

From all the summarised results on commitment and motivation, it is the concluded that there is a combined influence motivation and commitment which affects employee performance by 72%. Meaning that 72% of the employee performance variable can be explained by the work motivation and commitment variables, while the remaining 28% is influenced by other outstanding variables. It, therefore, means that the influence of motivation and commitment on employee performance is either direct and indirect. The concluded findings reveal that the direct influence of work motivation on employee performance is greater than the indirect influence. In this research, the commitment has been found to be one of the major variables that affect the performance of employees both directly and indirectly.

In conclusion, we have established that there are many other variables that affect the performance of employees at work compared to the currently studied variables presented in this paper. It has been noted that work motivation and employee commitment in relation to the present study are appropriate because they can serve as bridging intervening variables or as an intermediary between the variables of good work discipline, positive re-enforcement in form reward, and individual capacity on employee performance.

5. DISCUSSION

Looking at employee performance at work leads us to a discussion on work which is a way human being actualise themselves within communities. Several studies on work have examined and explored a broad set of potential work performance [1] indicators and since satisfaction is the only way workers feel they have reached the level of actualisation [5, 6] it becomes a fundamental measure in employee performance.

Taxation being a tangible activity which is measured by how much is collected, then work in this line is in a tangible form calculated depending on the value of revenue collected. Kuiper and Janssen [7] pointed out that work from a tangible perspective in a taxation department is handled the way private banks and wealth managers operate. Rahman [15] notes that workers operate this way for Indonesia’s case is the desire to improve the taxation system. This is embraced with the aim of achieving intended taxation goals.

Work discipline is an attempt by the organisation to implement or enforce regulations on condition that an employee must follow the established company policies without exception. This is important for staff commitment and motivation if there is to be any accelerating growth and development [14]. In the UNDP human development report of 2013 [11], it is pointed out that efficient human resource is a fundamental aspect of the achievement of increased income [13] for the country.

Discipline is an attitude and behaviour that is in accordance with the rules of the company [24] which is required to ensure a healthy [20]. Taxation workforce is required to maintain good performance [22] when this is perceived from an organizational perspective, it is interpreted as being obedient of every member in the company, following the set rules and regulations. According to Ledger et al [21], such a measure includes deterrence in policy, which acts as a suitable strategy in promoting tax payment by citizens. The tax revenue collected acts as evidence [22], since, there is an expansion of the tax base which is because of avoiding the poor behaviour.

Based on data processing results, work discipline as a variable has a certain degree of contribution to motivation. This means that workers, with good discipline at work, contribute to good organisational performance. This influences compensation received by employees from their employer. On this note, it is supported by Itner and Larcker [1]; Soegoto and Narimawati [2] who point out that work performance depends on potential performance measures and nature of the work. This means that several of the respondents already have a fairly good level of work discipline. This was evident from employee answers about always being present in any situation and condition at work. Motivation and commitment can help to dislodge and prevent linkages [13] hence providing a proof of how important disciplined workers may contribute to good performance.

Going by the constitution on taxation and discipline of employees who are kin to government regulations on civil service article No. 53 of 2010 and article on discipline No. 30 of 1980 find it critical to achieving expanded tax revenue and improved economic growth. They follow the rules and adhere to the changed tax collection system from official assessment to self-assessment [15]. The rules may carry a punishment if not observed or violated by any given employee. Such disciplinary offences maybe in verbal communication, written or in action by a given civil servant. In such a situation, proper regulations work to deter uncertainties caused by some other factors, consisting of intrinsic or extrinsic motivations [16].

5.1. Positive Re-Enforcement in the form of Work Compensation

The term compensation can be defined differently. From an insurance perspective, it refers to costs’ replacement and other benefits, which form as a reward to good performance at work by employees to their workers. It is one of the factors which determine whether it is viable to continue or leave a given job. On this point, Hofmann, Hoelzl and Kirchler [18] suggest that taxpayers’ willingness to cooperate with the government and its institutions is one form of the variable that arises from compensation. As workers are committed to service delivery, it is evidence of the importance of compensation in any organisation.

Though compensation is mostly used to refer to insurance benefits, in this research, we refer to a way of reward to performing employees in a company. This means that compensation plays a fundamental role in the smooth running of a company. In other words, employee compensation represents all forms of payment or reward given to employees emerging from their work. Direct payments are payments in the form of wages, salaries, incentives, and bonuses, and indirect payments are payments in the form of financial benefits such as insurance premiums [1, 2, 3, 5].

A compensation program, if well regulated, helps the organization in achieving its goals as well as increasing earnings, maintenance, and enhances productivity among workers [1-26]. It has been suggested that the more committed and motivated workers are, the higher the probability of achieving the established organisational objectives, hence enhancing work performance [19]. This implies that without good compensation, employees may be forced to leave the company. It is, therefore, concluded that each company should arrange for the provision of a good compensation program if it is to maintain mutual benefits to both employees and the company.

Going by the interpretation and analyses made from the study, compensation is categorised as average lying in between the category of good to very good. This suggests that most respondents are still not satisfied with the compensation they have so far obtained. Hence, showing that the taxation department in South Kalimantan has not yet followed the rule of ensuring a healthy [20], and efficient working environment which is supported by the existing motivation and commitment of the staff who are a fundamental component in tax collection [21].

5.2. Individual Capacity (i.e., Competence)

Individual ability is an important factor which determines work performance of the employees- who look at being competent as an individual pride within the public or any private organizations. Due to the uncertainties, caused by some other factors, which may include poor remuneration of workers, individual ability is an important factor which plays an important role [2, 15, 16]. To be competent, one should be knowledgeable since competence is a skill possessed because of one’s knowledge which is supported by work attitude and practical application during work.

According to UU 1945 [8] in Indonesia, competence is an individual capability with clear characteristics possessed by any civil servant in the form of knowledge, attitude, and behaviour, demonstrated during work. It has been found that many studies on worker performance encourage establishing a broad set of potential performance measures as determinants between workers [1] and corporations.

Going by the survey findings and analysis, competence of the human resource encourages individual workers to work towards achieving expanded tax revenue and improved economic growth. In the human development report of 2013, it mentioned that with efficient human resource countries such as Indonesia, can accelerate their achievements [11] at all fronts including tax expansion. It is because worker of the taxation are aware of the fact that they are a public asset and therefore strive to offer the best service to the country.

5.3. Work Motivation

Motivation may refer to a mental status of an individual which encourages and enhances individual performance at work. A motivated worker is critical to achieving expanded tax revenue by a country because there are no leakages arising from conspiracies and intrigues between rogue taxpayers and rogue tax officials, hence preventing fake finance validation [13]. Going by the suggestions from motivation experts, it can be concluded that there is no motivation without the feeling of need and satisfaction. As motivation consists of both intrinsic and extrinsic motivation [2], whereby intrinsic motivation which is also referred to as inner motivation plays a more fundamental role in enhancing employee commitment hence, performance.

An intrinsic reward is a self-actualisation reward which provides a feeling of satisfaction or being grateful and leads to emotions of high self-esteem and pride at work. Meanwhile, an extrinsic reward is external in nature it is from other individuals who tend to compliment on our performance. For instance, to praises from superiors or supervisors is a form of an extrinsic reward. Going by the descriptive analysis, in this current research motivation showed a good outcome, with an average category of pretty good to very good. This is an indication that workers feel that they are not fully motivated because they are not always invited to participate in decision-making, causing them to feel that their existence is unnecessary. Yet, the motivation of employees is necessary for carrying out tasks, which can lead to the achievement of organisational goals [16].

From the overall discussion, it has been established that employee survival will always thrive in a situation where individual workers fell attached to the organisation or company. Commitment and motivation are factors which influence productivity due to improved worker performance. However, other factors including proper regulations are required to avoid uncertainties during work.

CONCLUSION

Tax revenues in each country cannot be fully realized in accordance with the planned targets without good work, which is influenced by individual performance. The performance of employees includes the dimensions of quality of work, quantity of work, and loyalty or responsibility. However, there should be proper regulations due to the uncertainties caused by other factors, which may include increased and improved remuneration of workers. Motivation in employees is necessary for carrying out their tasks, which can lead to improvement of the company’s performance.

ETHICS APPROVAL AND CONSENT TO PARTICIPATE

Not applicable.

HUMAN AND ANIMAL RIGHTS

No Animals/Humans were used for studies that are base of this research.

CONSENT FOR PUBLICATION

Not applicable.

CONFLICT OF INTEREST

The authors declare no conflict of interest, financial or otherwise.

ACKNOWLEDGEMENTS

Declared none.